Own your path

Excited about what’s next?

Book a demo

You’re reviewing a rental application and the applicant can't link their bank account directly through services like Plaid. Maybe they use a smaller regional bank that doesn't integrate with these platforms, or they're simply uncomfortable sharing their online banking credentials. When direct account linking isn't possible, applicants need to upload PDF bank statements instead—which can open the door to fraud.

"There's two ways you can verify bank," explains Matt Lisowski, Director of Product at Findigs. "If you're bank linking, that's done. We don't have to worry about fraud. We know you've legitimately linked to a bank account, your name matches, you logged in. That's very different. If you're uploading PDFs, bank statements, things are handled totally differently."

The Federal Trade Commission has taken action against multiple operations that openly sold fake financial documents to consumers. In 2018, the FTC shut down websites selling "authentic looking" fake bank statements, pay stubs, and W-2s from templates of five well-known U.S. banks. This enforcement highlights that the supply of fake documents is readily available online, contributing to the rising fraud problem.

Since bank linking isn't always possible for every applicant, property managers need effective ways to verify uploaded statements without creating unnecessary delays. The goal is to catch the small percentage of manipulated documents while keeping your approval process efficient for the majority of honest applicants. Here’s what to know about how to identify fake bank statements without slowing down your entire process.

Creating convincing fake documents used to require serious technical skills. Not anymore. "The tools of manipulation are pretty omnipresent," Lisowski notes. "Before, maybe you had to know how to use Photoshop pretty well or something like that. And now it's much, much easier."

The accessibility of editing tools means someone can take a legitimate bank statement PDF and modify balances, transactions, or account details in minutes. What makes this particularly challenging is that many altered documents look completely authentic at first glance. Many people attempting this aren't career criminals. About 45% of fake documents come from people using their real identity but inflating their financial details to meet rental requirements.

Many fraudulent bank statements today look surprisingly real and will be difficult to catch by manual review. However, not all will be doctored with the same level of sophistication, and there some signs your team can look out for that something might be off:

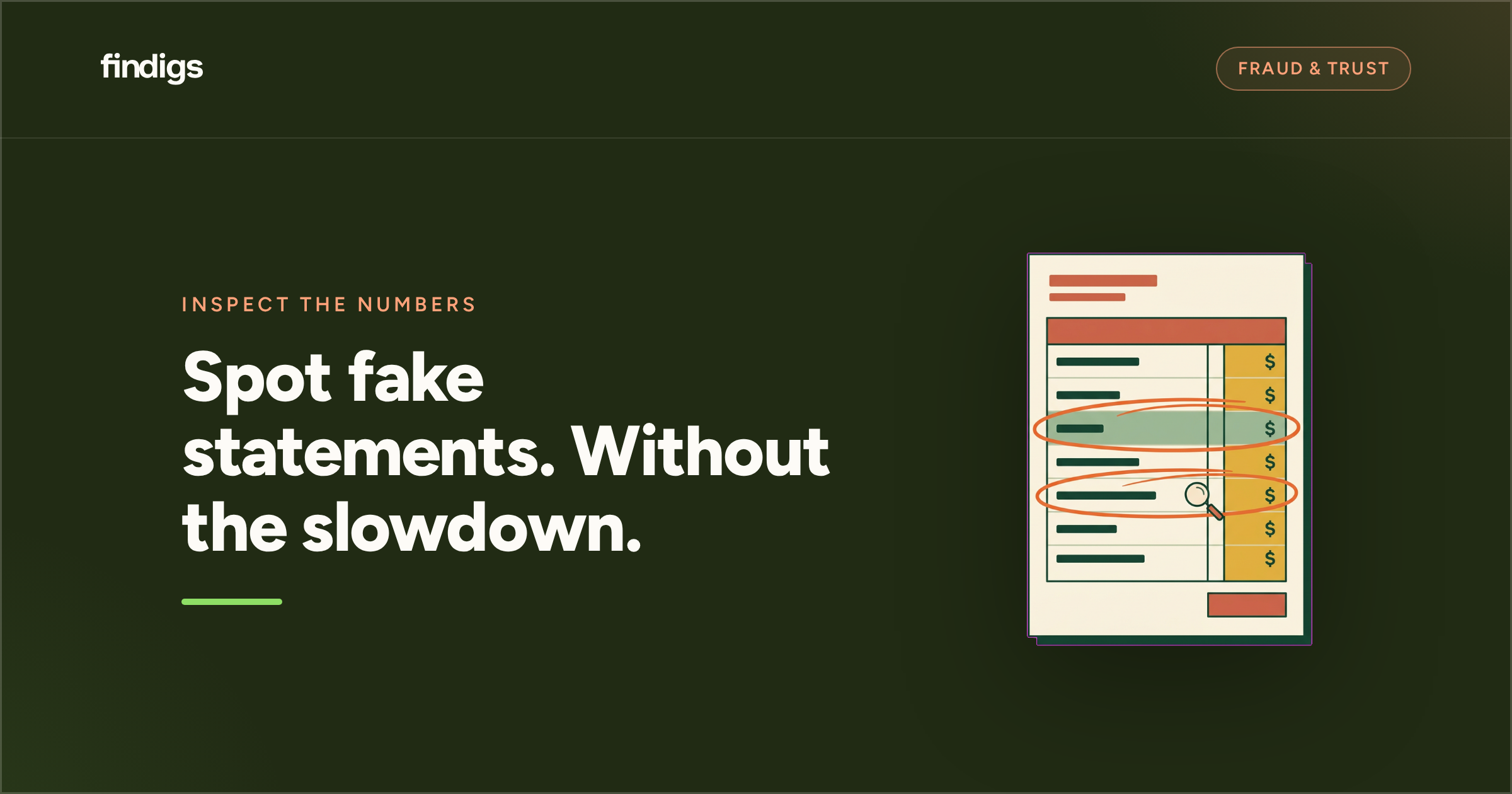

Start with the basics: do all the numbers add up? Opening balances plus deposits minus withdrawals should equal closing balances. This seems obvious, but it's one of the most reliable checks you can do. "If we sum them all up, and it doesn't match to the bottom, that’s an issue" Lisowski explains. Since banks use automated systems that don't make calculation errors, any arithmetic mistakes usually indicate human tampering. However, this can be time-consuming to check for manually.

Real bank statements follow strict formatting standards. Look for mismatched fonts, unusual spacing, or logos that seem off. Even subtle differences—like one page using slightly different typography—can indicate editing. Professional documents from major financial institutions don't contain typos or grammatical errors, so these are immediate warning signs.

Pay attention to the transaction history itself. While legitimate paychecks may show identical amounts, look for suspicious patterns like multiple transactions using the same reference numbers, or large deposits that conveniently appear just before application submission. If you receive pay stubs alongside bank statements, verify that direct deposit dates and amounts match between documents.

Every page of a legitimate statement series should show consistent account holder names, account numbers, and bank details. When these details vary across pages—different spellings of names or changing account numbers—you're likely looking at a manipulated document.

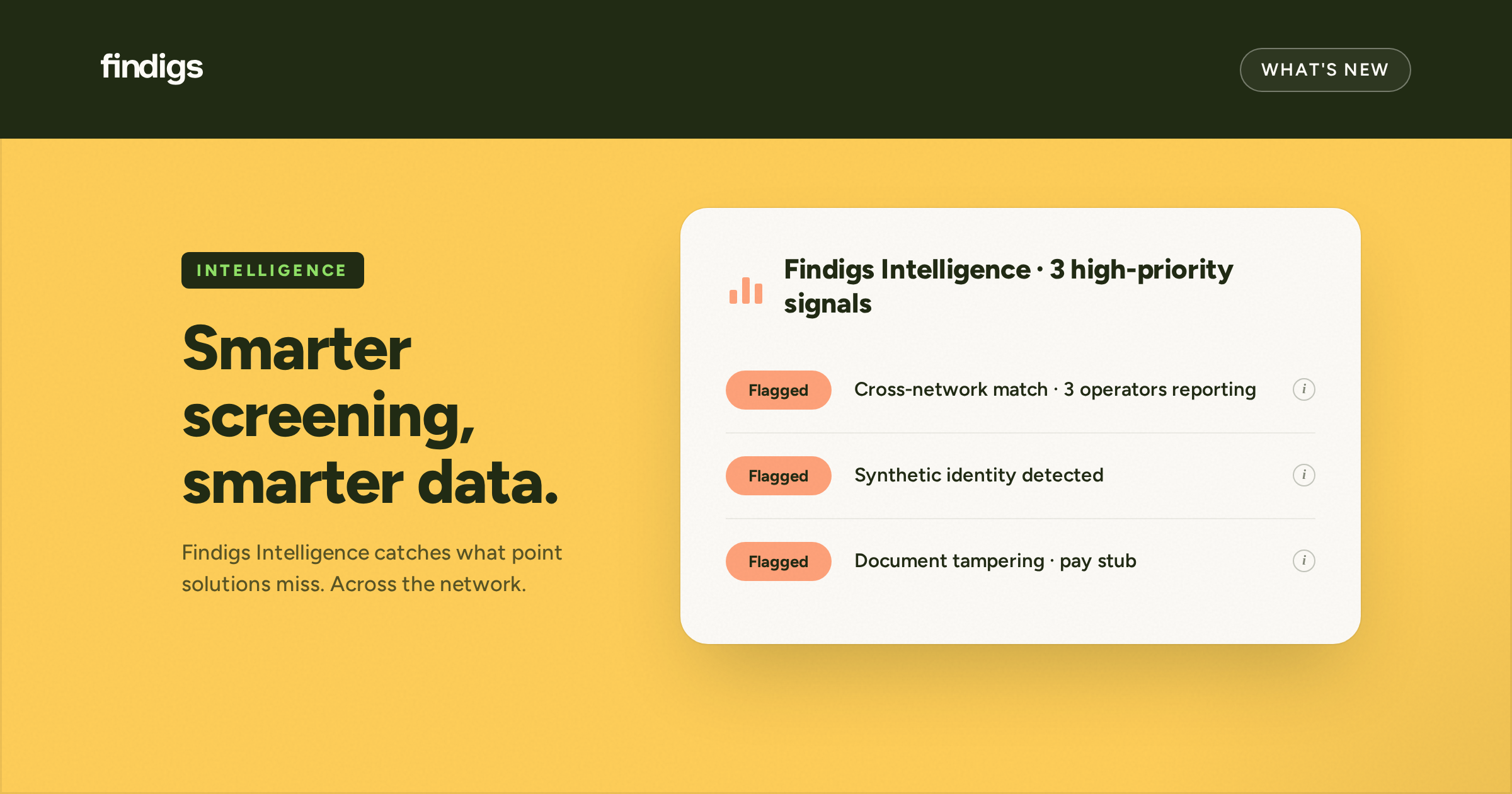

Many document manipulation signals have become completely invisible to manual review. Document metadata—the hidden file properties—can reveal key information about how and when a document was created.

"We're looking at the metadata associated with it," Lisowski explains. "We're looking for signs of document manipulation—things that may be hard to spot with the naked eye, but when we're running it through, it might be able to say like, 'oh, this particular transaction is off by like 2 pixels compared to the other one.'"

Banks generate statements using specific software, so when metadata shows creation by image editing programs, that's a flag. Similarly, statements dated months ago but showing recent modification timestamps indicate possible alteration.

"There's an online first bank where we noticed a lot of fake statements being submitted,” Lisowski shares. “The metadata on these documents kept showing the same place that they were generated from—a place that real statements from this bank would never have been generated from." This pattern allowed fraud detection systems to flag these suspicious statements for additional review.

Today’s fraud detection systems perform analysis that goes beyond what human reviewers can accomplish—and does so faster and more reliably. These systems excel at spotting patterns across thousands of documents and identifying subtle inconsistencies.

Automated systems maintain extensive libraries of genuine bank statement formats, comparing uploaded documents against expected layouts, fonts, and security features. They can detect minute deviations in logo placement, margin spacing, or typography that would be nearly impossible for a human reviewer to catch consistently.

When someone uses an online generator to create fake bank statements, these tools may reuse the same underlying data across multiple documents—including transaction reference numbers. Transaction IDs are the unique reference numbers that banks assign to each deposit, withdrawal, or transfer—think of them as digital fingerprints for every financial transaction. Automated systems can instantly compare transaction IDs across thousands of applications and flag when the same "unique" numbers appear repeatedly.

"If there are fake bank statement generators that are really good and they generate transaction IDs, those IDs are the same every time," Lisowski explains. A human reviewer may never notice repeated transaction IDs across hundreds of applications, but technology solutions today are built to flag these patterns.

The most reliable verification involves comparing bank statements against other documents in the application package. When applicants submit pay stubs alongside their bank statements, for example, the direct deposit entries should match—same employer name, same amounts, same dates. Any discrepancies often reveal manipulation attempts.

When manipulated bank statements slip through your screening process, the consequences extend beyond the initial deception. Property managers report writing off $4.2 million in bad debt annually on average, with roughly one-quarter attributed to fraud-based nonpayment. But there's also the hidden cost of time—while your team spends hours manually reviewing suspicious documents, qualified applicants may find faster approval processes elsewhere.

Protecting against document manipulation requires a layered approach. Think of it like building a security system—multiple checkpoints work better than relying on any single method.

Collect multiple documents: Requiring several forms of financial proof makes comprehensive falsification much more difficult. Bank statements should align with pay stubs, tax forms, and employer verification letters. Inconsistencies between documents often reveal manipulation attempts.

Continually apply best-in-class technology: Fraud techniques are always evolving, so your technical solutions need to keep pace. Automated verification systems handle high volumes while detecting minute inconsistencies invisible to manual review. These tools check metadata, compare document formats against known templates, and identify suspicious transaction patterns—but they must be continuously updated to stay ahead of new manipulation methods.

Keep your team informed: Make sure staff understand that sophisticated document manipulation exists and know the warning signs. Even basic awareness helps reviewers stay alert to potential issues.

Verify through original sources: When possible, request documents directly from financial institutions or employers. Some banks offer secure delivery methods or verification codes that help confirm authenticity.

Cross-check everything: Direct deposits shown in bank statements should match pay stub information exactly. Listed employers should confirm employment when contacted.

As Lisowski puts it: "It's not just one piece, but it's all these things together oftentimes that signal something is more likely to be fraudulent."

At Findigs, bank statement analysis is powered by our proprietary document analysis engine that automatically examines every uploaded PDF for signs of tampering or fraud. But what makes our approach especially effective is how this analysis integrates with our complete fraud detection system.

When someone uploads a bank statement, our AI-powered engine immediately scans the document for fraud indicators—the kinds of manipulation signals that Lisowski described, like metadata showing creation in image editing programs or transaction details that are misaligned by just pixels.

Fraud signals from other parts of the application can trigger closer examination of bank statements, and vice versa. If our identity verification raises questions, or if behavioral patterns during application submission seem suspicious, those red flags prompt our system to take a more detailed look at the financial documents. Conversely, if our document analysis detects potential tampering in a bank statement, that signal can trigger deeper review of other application components.

The results appear in an intuitive dashboard with simple next-step suggestions, so reviewers can quickly understand what they're seeing and how to proceed.

Document manipulation of all types is on the rise, from bank statements to pay stubs to identification—driven by the widespread availability of editing tools and online services selling fake documents. This puts pressure on leasing teams to become fraud detection experts, but focusing too heavily on catching manipulation can slow down your approval process and create delays for legitimate applicants.

Technology can help solve this challenge. At Findigs, we first try to connect applicants directly to their bank accounts through secure linking, which eliminates the bank statement fraud issue entirely. When that's not possible, our comprehensive fraud detection system automatically analyzes uploaded documents while also examining identity verification, behavioral patterns, and cross-referencing information across the entire application.

Want to learn more about how a holistic approach to fraud detection can help you catch suspicious documents and other vulnerable points in your screening process? We’d love to chat with you about how we can help.