Own your path

Excited about what’s next?

Book a demo

Property managers routinely review rental submissions that fall short of meeting income, credit, or employment standards. In these cases, leasing teams often require an additional financially responsible party to support the application by filling in the gaps. Cosigners and guarantors are the two most common solutions.

Stakeholders sometimes use the terms interchangeably, even though they entail different legal obligations, approval workflows, and collection procedures. When leasing teams understand those distinctions, they can apply consistent policies competently, minimize bad-debt exposure, and make leasing decisions faster.

This article walks property managers through how to structure reliable, hassle-free rent rolls that consistently meet cash flow expectations.

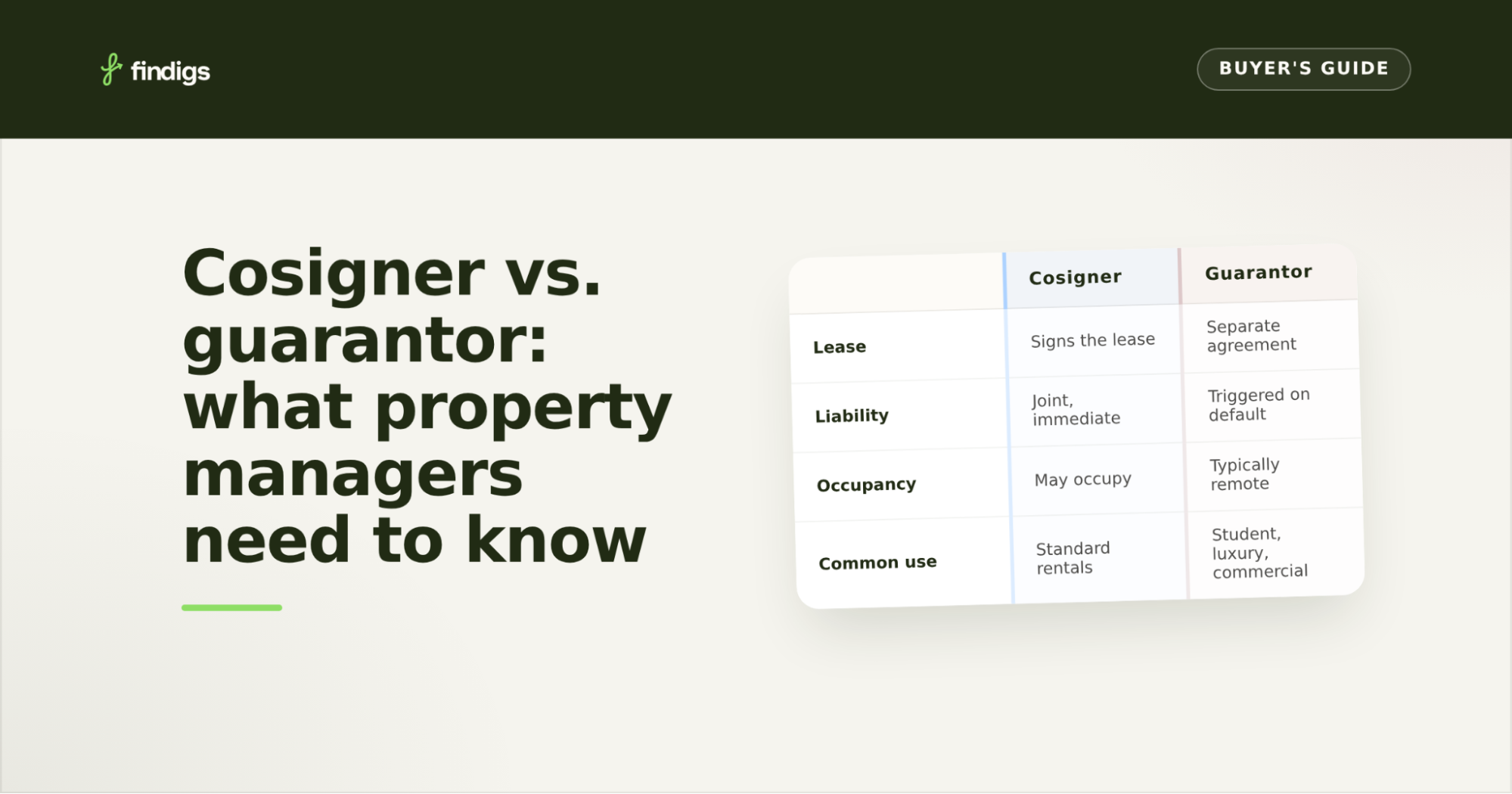

A cosigner is a third party who signs the lease alongside the renter and accepts joint and several financial responsibility for the lease obligations. This means that if a delinquent tenant misses weekly or monthly payments or violates the lease terms, the cosigner can be held responsible for all debt, collection activity, and related legal costs.

Lease applicants typically call on cosigners when they cannot meet the tenant qualification requirements on their own. Instead, the leasing team relies on the cosigner’s higher income, stable employment history, or stellar credit profile to support the would-be renter’s application.

In most residential leasing situations, cosigners either occupy the unit with paying renters or maintain a close personal relationship with them.

A guarantor is a person or an organization that agrees to cover the lease obligations if the lessee defaults on payments. Unlike a cosigner, a guarantor does not sign the lease alongside the primary lease applicant, and thus has no direct lease rights and usually does not occupy the property.

A separate guaranty agreement or guarantor addendum tied to the lease, taking state laws into account, governs the guarantor’s liability. Lease structures still determine when a payment failure has occurred and guarantee obligations become enforceable.

These parties are common in more complex leasing situations, such as student housing, luxury homes, commercial settings, and relocation housing. In many cases, it involves applicants who, for various reasons, cannot meet the screening thresholds on their own or even with a cosigner.

Although both roles support lease applicant qualification, they operate differently from both financial and operational perspectives. Consider the following categories for a comprehensive comparison:

Rental network managers who fail to distinguish between these roles often encounter erratic qualification workflows and collection procedures across properties.

Cosigners are most useful when applicants demonstrate some strong renter qualifications but lack others. As a result, they can’t secure a desirable lease on their own. Typical cosigner candidates include would-be renters who have:

For large residential rental networks, cosigner policies also help standardize qualifications across approval staff and locations.

Guarantors are usually required when the applicant’s qualification gap is larger or more complex, and for many property categories other than single-family homes. Common situations include:

In many cases, guarantors help operators approve otherwise qualified applicants while maintaining portfolio risk controls.

Leasing professionals must verify that cosigners and guarantors can realistically absorb the lease obligations they agreed to if the renter defaults. The following are the most favored methods:

Leasing managers typically review:

Guarantors are often held to stricter income requirements, typically 4x to 6x the monthly rent.

Criminal-intent risk increases when multiple parties are involved in an application. Stakeholders in this business should be wary of encountering:

Standardized identity verification and fraud-detection procedures support operators’ efforts to reduce bad-debt exposure across large property holdings.

Operators commonly review:

These evaluations should align with documented screening policies to reduce inconsistencies in approvals for regional managers and operators.

Most leasing organizations establish metrics and yardsticks for:

Clear qualification rules encourage leasing teams to make faster, more centralized decisions to secure the best renter selections during high-volume leasing periods.

Cosigners and guarantors provide significant occupancy flexibility and leverage. Simultaneously, they can lay the groundwork for future operational and compliance challenges if policies are disorganized or display compliance weaknesses. The most prolific examples of these are:

Lease language may seem like a “copy/paste” exercise, but that’s a misconception. It requires forethought to anticipate complications that arise from including multiple parties in the rental mix. Without this, financial responsibility when activating collections, enforcing leases, and issuing legal notices can become operationally difficult and legally non-compliant. Consistent lease language across all property holdings mitigates unexpected and unwanted malfunctions in these areas.

As highlighted above, the likelihood of criminal intent increases when multiple parties provide supporting documentation. Proven digital review systems are fast replacing manual processes in detecting sophisticated schemes and deviant patterns.

Property strategists frequently fall into the trap of treating each rental component in the network as a separate business with its own policies. For example, one leasing agent may approve a guarantor-assisted application, while another may reject a nearly identical one. Operational inconsistencies align with increasing inefficiencies, lost revenue, erratic cash flows, and potential fair housing concerns.

Different property types align reliably with distinct leasing decision structures, yielding the best results based on renter demographics and portfolio risk tolerance.

Manual cosigner and guarantor reviews are prone to inconsistency, documentation overload, and subjective leasing decisions that vary by reviewer and location. The following practices help leasing teams apply more consistent, defensible standards across every application.

Manual cosigner and guarantor review is one of the most time-intensive stages in the leasing process. Findigs replaces that manual pass with automated decisioning that applies operator-defined policies consistently across every application, including those involving additional financially responsible parties.

Cosigners and guarantors both support units-for-rent operators in approving lease applicants who fall short of underwriting requirements. Still, their inclusion in the solution requires addressing the diverse financial obligations and processing responsibilities associated with these entities.

Time pressures, managerial subjectivity, the stress of flawed criminal detection, and inconsistency between property sub-teams are constant obstacles to improved property management performance.

Findigs, the decisioning platform for residential leasing, addresses these pain points by enabling faster, more confident decision-making, while improving operational consistency and reducing manual review burdens. The net result is faster decisions, more consistent enforcement of screening criteria, and stronger protection of revenue quality across the leasing process.

Yes, using the same qualification criteria for both can create unnecessary risk and inconsistent approvals.

Learn more about Findigs policy optimization solution.

Sometimes, but only when portfolio policies explicitly allow it.

The most common mistake is inconsistent policy enforcement between reviewers, properties, or regions.

Discover how automated screening helps property managers uphold fair housing laws.

Every additional applicant, cosigner, or guarantor increases the number of documents and identity signals that require verification.

Findigs applies operator-defined policies automatically instead of requiring manual reviewer interpretation.

Discover how Findigs helps you leave manual reviews behind.