Own your path

Excited about what’s next?

Book a demo

The single line item that decides whether a qualified renter signs this week or walks to the next listing is the pay stub. Operators feel the pressure on both ends of that step. Speed-up requests come from leasing teams, and accuracy demands come from the underwriting side, because fabricated income documents are now the most common rental-application fraud category.

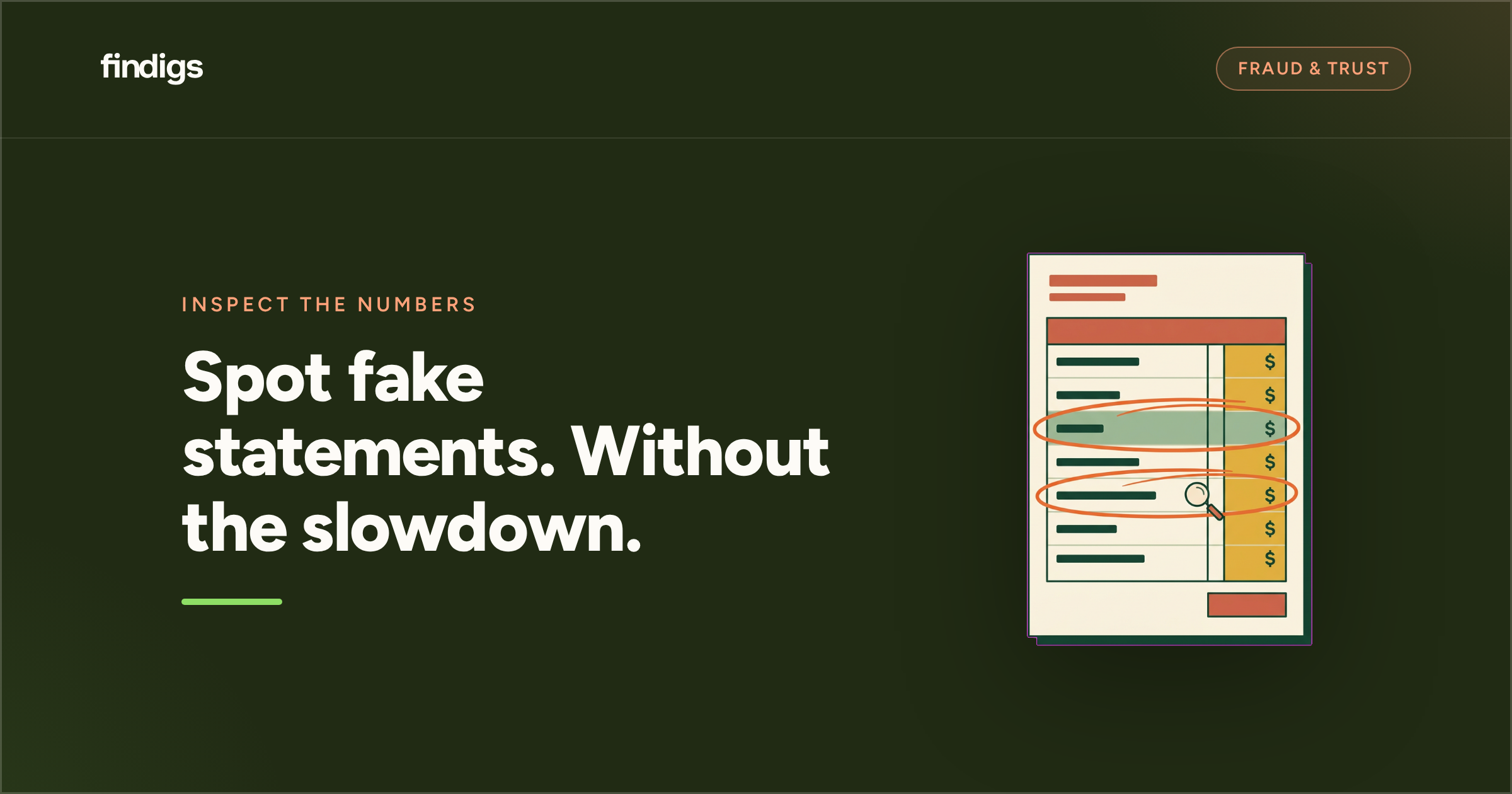

Verifying a pay stub comes down to four checks: confirm the employer and employee details match the application, pay frequency and period dates are internally consistent, gross minus deductions equals net pay, and confirm year-to-date totals reconcile to the current period.

This article walks through each check, then covers the red flags that surface most often, the income documents to accept when an applicant does not have traditional stubs, and how automated decisioning collapses the manual pass into a same-day yes or no.

Pay stub verification is the process of confirming that the income an applicant reports matches what their employer paid, by cross-checking the stub’s line items against employer records, bank deposit data, or third-party employment feeds. The check sits inside the Fair Credit Reporting Act’s permissible-purpose framework, which limits the data collected to the suitability decision and requires the applicant’s written authorization. AI-generated income documents have raised the stakes on every manual pass, with one industry experiment finding 74% of AI-generated fake IDs passed optical card readers, and the same generators now produce convincing pay stubs.

Verification is triggered at every income-relevant decision point: a new application, a renewal that re-qualifies income, evaluation of a co-signer, and recertification on income-restricted units. The Consumer Financial Protection Bureau frames the activity as a core function of tenant screening, run through either manual employer outreach or automated employment data feeds. The same written screening authorization covers contacting the employer named on the stub.

A complete verification pass takes four steps, each anchored to a specific zone of the pay stub:

Confirm the legal employer name, the EIN when shown, the employee’s name, the last four digits of the Social Security number, and the pay period and date. Each should match the application exactly. Template farms and AI-generated employer blocks are now common enough that leasing teams encounter fabricated employer details on a regular basis.

Identify the pay frequency (weekly, biweekly, semimonthly, or monthly per Bureau of Labor Statistics conventions) and confirm the period dates align with that cadence. A biweekly stub dated outside a fourteen-day cadence is an inconsistency worth resolving.

Net pay should equal gross pay minus the listed deductions, and tax withholding should be plausible for the wage and state. A net-pay figure that misses by more than a rounding cent, or a federal withholding implausibly low for the wage, points to either a payroll error or a fabricated document.

Year-to-date gross should equal current-period gross multiplied by the pay periods completed, allowing for mid-year hires. YTD totals that fail to reconcile are one of the most documented signals of editing on otherwise convincing stubs, and remain the single check most reliable against template-generated forgeries.

The four categories below cover the dominant fabrication patterns, also documented in the 2026 Risk Management Magazine analysis of apartment rental fraud:

Reviewing a single document at the application stage is rarely enough on its own. More than 70% of respondents to a 2024 NMHC survey reported an increase in fraudulent applications and payments in the preceding 12 months. Rental fraud costs are often passed downstream: operators raise rents to recoup bad debt losses, which means qualified renters bear the financial impact of fraud they had no part in.

Request two or three consecutive stubs and verify that the employer, deduction structure, and year-to-date progression line up across periods. The FBI's 2025 Internet Crime Report tracked roughly $275 million in reported rental fraud losses across more than 12,000 cases in 2025 - a reminder that single-stub review leaves money on the table.

Match the net-pay figure on each stub to a deposit on or near the pay date in the applicant’s bank statement. Recurring direct deposits from the named employer corroborate the stub, and a mismatched deposit cadence is worth following up on through a structured income verification request.

Look up the employer through a state corporate registry or independent business directory rather than calling the number printed on the stub. AI-built fraud rings now stand up convincing employer websites and answering services specifically to corroborate fake stubs, as outlined in Findigs’ May 2026 analysis of FBI rental fraud data.

A written rent-to-income standard (commonly 2.5x to 3x monthly rent) applied uniformly across every applicant reduces Fair Housing exposure and makes the audit trail defensible. The standard belongs in a centralized screening policy, not in any reviewer’s memory.

Roughly 64 million Americans were freelancing or in non-traditional work in 2023, around 38% of the workforce per Upwork’s 2026 freelance economy data, so a meaningful share of applicants may not have traditional biweekly pay stubs.

Income document types and what they verify:

Findigs is the residential leasing decisioning platform for property managers, the only one that delivers an automatic yes or no on every rental application. It helps operators fill more units and collect more of what they lease - the outcome Findigs calls revenue quality. Screening, underwriting, and decisioning run on one platform, so the four-step manual pass ends in a decision, not a score or a flag.

Manual pay-stub verification is no longer just an administrative step. It is now one of the most critical fraud checkpoints in the leasing process. AI-generated income documents, fake employer identities, and increasingly sophisticated rental fraud schemes have made traditional visual review unreliable on its own. At the same time, leasing teams cannot afford multi-day approval cycles that push qualified renters toward competing properties.

Findigs solves both problems at once. Instead of relying on disconnected screening tools and manual verification queues, it combines income verification, fraud detection, underwriting, and decisioning into a single automated workflow. Employer data, bank-side income signals, and network-wide fraud intelligence are evaluated simultaneously to return an automatic yes-or-no decision in a median of 3.4 hours.

The result is faster approvals, stronger fraud prevention, and less operational burden on leasing teams. While other platforms stop at scores or flags, Findigs delivers a fully backed leasing decision built for the realities of modern rental fraud, protected by a contractual fraud guarantee that no other vendor in the category offers.

Most operators should request two to three consecutive pay stubs to validate income consistency and reduce fraud exposure.

Learn how to reach full-spectrum income intelligence with Findigs.

The fastest verification workflows combine automated income verification with structured fraud checks instead of relying on manual visual review alone.

Find out how to get to a one-day resident screening decision.

The most common fraud indicators are inconsistent math, unrealistic withholding amounts, and employer details that fail independent verification.

Explore how AI can generate fake pay stubs.

Non-traditional income applicants should be evaluated using deposit consistency, tax documentation, and verified banking activity rather than traditional payroll assumptions.

Findigs automates pay stub verification by combining employer data, bank-linked income validation, document analysis, and fraud intelligence into a single decisioning workflow.

Explore Findigs’ fraud protection solution.